Real-time Payments:

Tokenized deposits can facilitate real-time payments between consumers, businesses, and merchants.

Bringing blockchain innovation to the real world through the creation of blockchain native bank payment rails.

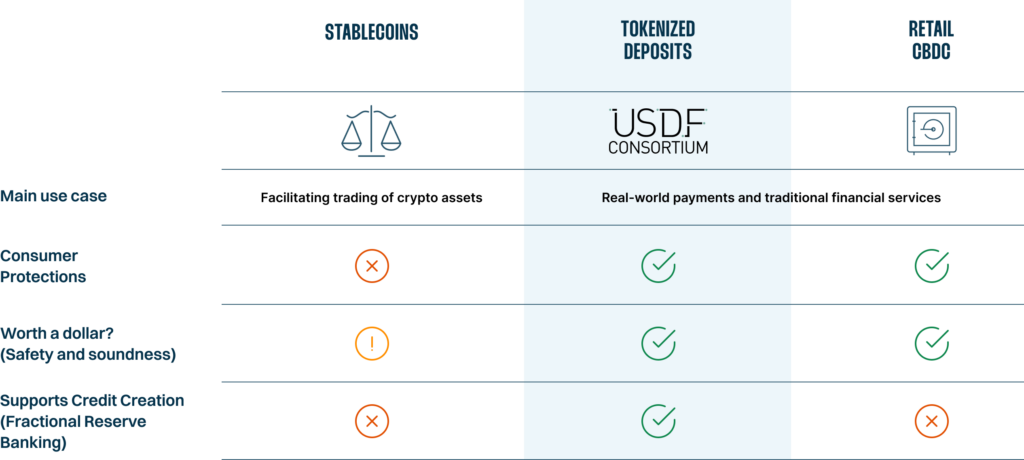

USDF is the banking industry’s answer to the need for a digital dollar. Blockchain technology can make payments more efficient and improve traditional banking services, expanding access to safe and affordable financial services.

Most money in the US economy today is held as a deposit at an insured depository institution. The vast majority of this is held digitally. The Fed estimates that just 6% of transactions today are in cash.

We believe that the best way to leverage blockchain technology is to extend the existing banking model into this tokenized environment.

11%

Notes and Coins

16%

Reserves accounts at the Fed

73%

Bank deposits

As we bring money onto blockchain, we must maintain the numerous benefits and protections that our banking system provides today.

that delivers modern payments infrastructure while maintaining the numerous protections and benefits that our two-tier banking system provides today.

Bank-Owned

The USDF Consortium is owned by its member institutions.

Real-world value

USDF is focused on bringing blockchain innovation into the “real world” by leveraging blockchain technology to improve traditional banking services rather than facilitating engagement in the non-bank crypto ecosystem.

Open platform

USDF is an open platform for innovation. Banks have the freedom to use USDF payments to power any application of their choosing and can elect to integrate to the chain through any vendor they choose via open-source code. Banks will never have to hire a specific vendor or implement or engage with USDF.

Interoperability

The USDF Consortium was founded to provide a forum for banks to come together and discuss common standards for blockchain-based payments. Today we see the development of many closed-loop systems that struggle to talk to each other. Without interoperability, these systems will never deliver the promise of more efficient payments.

Supports Credit Creation

USDF allows banks to leverage blockchain technology while ensuring banks can continue to leverage deposits to power lending.

Blockchain technology holds tremendous promise to improve financial services, offering faster, cheaper services that can help promote financial inclusion, drive economic growth, and support the role of the U.S. Dollar as the global reserve currency.

USDF is the banking industry’s answer to the need for a digital dollar. Blockchain technology can make payments more efficient and improve traditional banking services, expanding access to safe and affordable financial services.

USDF is the banking industry’s answer to the need for a digital dollar. Blockchain technology can make payments more efficient and improve traditional banking services, expanding access to safe and affordable financial services.

Tokenized deposits can facilitate real-time payments between consumers, businesses, and merchants.

Programmable payments can automate payments flows to respond to real world events speeding up delivery of payments, creating efficiency, and reducing the risk of error or fraud.

Blockchain can serve as the ledger for other traditional banking assets such as loans. Bringing these assets on-chain can add transparency and make it easier to buy.

USDF represents banks of all sizes and advocates for regulatory clarity that ensures banks can leverage novel technology to be the responsible, trusted, and regulated provider of blockchain innovation.

Member

Connect with peer banks as you build your bank’s blockchain strategy, upskill staff through participation in working groups, and engage in industry advocacy.

Owner

Owners of the Consortium are working together to build common infrastructure and intend to operate USDF payments. This includes access to common infrastructure and shared legal resources related to the implementation of tokenized deposits.

April 4, 2022

USDF Consortium on Roll Call

January 13, 2022

FirstBank Executive on Why Banks Are Launching a Consortium to Mint Stablecoin ‘USDF’

January 13, 2022

US Banks Form Consortium for a Stablecoin Launch

January 12, 2022

US Banks Form Group to Offer USDF Stablecoin

January 12, 2022

U.S. Banks Back New Stablecoin

January 12, 2022

Community Banks Band Together to Issue Another Crypto Stablecoin

January 12, 2022

Banks Form Consortium to Mint USDF Stablecoins

January 12, 2022

Bank Stablecoin Consortium USDF Launched by NY Community Bank, Figure, Others

January 12, 2022

USDF Consortium Challenges Paxos with First US Bank-Minted Stablecoin

January 12, 2022

US Banks Plan USDF Stablecoin

January 12, 2022

USDF CONSORTIUM™ Launches to Enable Banks to Mint USDF Tokenized Deposits

November 22, 2021

Stablecoin Advocates Make Their Case to US Banking Regulators

September 13, 2021

New York Community Bank Announces Blockchain-Enabled Payment Processing, Secondary Trading